Класация на доставките на модули в световен мащаб за 2024 г.: значителна разлика между производителите

8. 3. 2025

8. 3. 2025

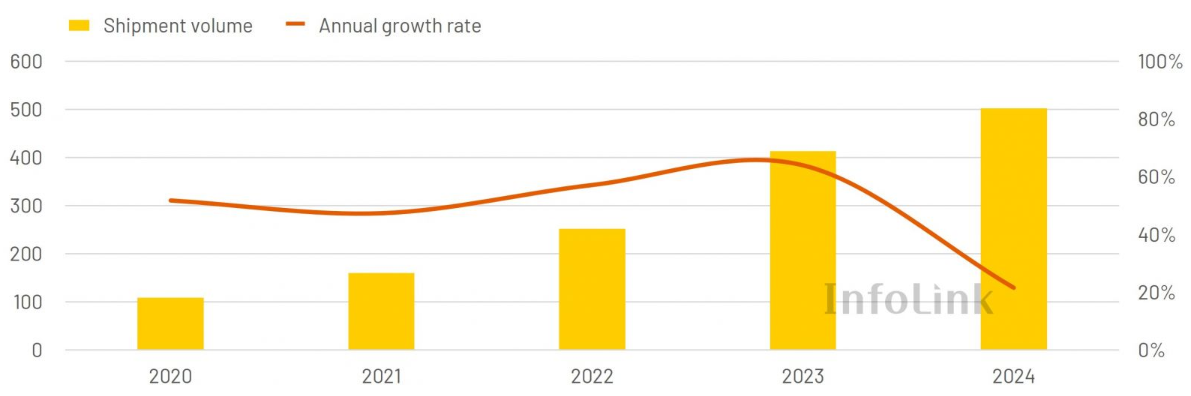

Compared to the previous year, the total supply of the top ten generators in 2023 was 413 GW, while in 2024 it reached 502 GW. Despite a 22% annual growth rate, sluggish demand and oversupply will prevent significant annual growth momentum in 2024.

The top four generators are close on the heels of each other in the rankings, while the differences between the other generators are more pronounced

According to InfoLink's 2024 statistics, the top ten manufacturers shipped approximately 502 GW of modules, representing a 22% year-on-year increase, indicating that the annual growth rate has begun to slow as previously expected, with Q3 and Q4 seeing less growth than in previous years.

Jinko, Longi, JA Solar and Trina continue to hold the top four positions, with a slight change in their ranking. Compared to the manufacturers ranked behind them, there is a significant difference in shipment volumes of over 30%, with the top four accounting for 63% of the total top ten volume.

Competition among the other manufacturers is very intense, the ranking is as follows: Tongwei, Astronergy, Canadian Solar, GCL, DAS Solar and Yingli. The difference between them is around 10 GW.

It is worth noting that DMEGC and Risen are tied for 11th place, each delivering 20 GW, which is close to 10th place. Starting from twelfth place, First Solar, Seraphim, Huayao and Hanwha show a larger difference in delivery volumes.

In general, we can see an increase in the share of Chinese manufacturers due to the support of stable Chinese demand.

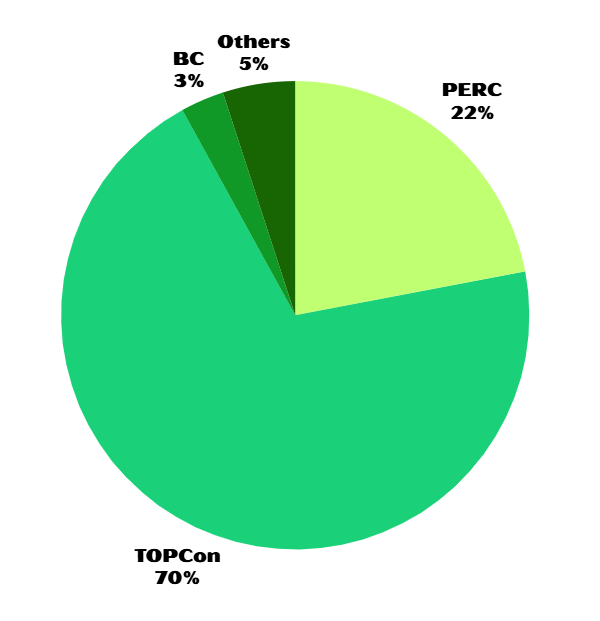

TOPCon dominates shipments

The top ten shipment figures show that PERC products account for around 22% of the total volume, while TOPCon n-type modules account for almost 70% of the total volume and BC products account for 3%.

Development in 2025

According to InfoLink statistics for this period, the total supply targets are set at 559-603 GW. Compared to the previous targets for 2024, the new targets reflect the manufacturers' move towards stability in their expectations for 2025. The n-type, HJT and BC expansion rates are projected to be close to saturation. However, according to the latest survey, some manufacturers indicated that they will adjust their targets based on order conditions or even set this year's targets with a focus on minimizing losses.

As self-regulation gradually came into effect at the end of 2024 to control production schedules, the decline in module prices has slowed. However, there are still a significant number of low-priced modules on the market, pulling the average price down.

InfoLink believes that in order to break through in a competitive environment, manufacturers need to place more emphasis on product quality.

In line with last year's theme, module performance, quality and efficiency are among the key factors that manufacturers can use to differentiate themselves. In addition, the ability to anticipate and respond to policy changes can give manufacturers a competitive advantage. In particular, geopolitical risks at the domestic and international levels need special attention this year.